In today’s digital-first world, banks and financial institutions face a paradox: legacy systems still hold essential business value, but the architecture around them struggles to meet the demands of modern digital channels like mobile and web.

Legacy systems are not a problem, legacy architecture is. These systems still contain valuable business logic and data, but it’s the outdated architecture around them that holds organizations back, making change slow, costly, and risky.

This is where the Digital Integration Hub (DIH) comes in.

What is Digital Integration Hub (DIH)?

A Digital Integration Hub (DIH) is a modern architectural pattern that centralizes data from various sources to provide a scalable, high-performance, and real-time data layer for digital applications. It acts as a central point for data ingestion, transformation, and distribution, offering a unified view of data across the enterprise. Digital Integration Hubs (DIHs) are particularly useful for enterprises undergoing digital transformation, enabling them to modernize legacy systems and improve customer experiences.

It collects, aggregates, and refreshes operational data from multiple sources — core banking, card systems, payment engines, scoring services — and makes it available through modern APIs that are fast, reliable, and developer-friendly.

This gives organizations the best of both worlds:

- Continue using reliable systems of record for transactions and compliance.

- Launch digital products rapidly, without waiting for massive migrations.

Why Digital Integration Hub (DIH) Is Essential for Modern Banking (and Beyond)

Modernizing legacy systems doesn’t have to mean replacing them. Digital Integration Hub (DIH) offers a safer path—extending the value of existing systems while enabling agile, incremental transformation.

Customers Expect Speed and Consistency

Digital Integration Hub (DIH) delivers a unified digital experience by abstracting complexity across multiple back-end systems. No matter how fragmented the core, users get fast, reliable service.

Scalability and Availability Are Non-Negotiable

Digital Integration Hub (DIH) ensures 24/7 performance and high-performance, elastic scalability—critical for both customer satisfaction and operational resilience.

Simpler Architecture Means Faster Development

Instead of managing 6–10 APIs, developers get a single, real-time data layer—cutting integration time, reducing cost, and accelerating delivery.

Built for Compliance and Real-Time Risk Management

From PSD3 to fraud detection, Digital Integration Hub (DIH) supports real-time access, lower risk, and audit readiness—reducing capital requirements in the process.

Ready for the AI Era

Enterprise AI needs more than documents—it needs structured, operational data. Digital Integration Hub (DIH) connects AI models to real-time systems, powering next-gen use cases in service, personalization, and fraud prevention.

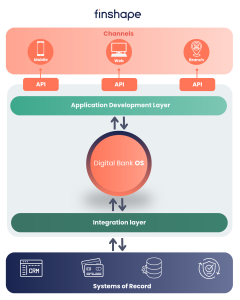

Digital Bank Operating System (DBOS) + Digital Integration Hub (DIH): A Winning Pairing for Digital-First Banks

Digital Bank Operating System (DBOS) is the execution layer that brings the Digital Integration Hub (DIH) concept to life. While Digital Integration Hub (DIH) is the architectural pattern, Digital Bank Operating System (DBOS) is the productized platform that conforms to it—out of the box.

Here’s what that means:

- Digital Bank Operating System (DBOS) is the Digital Integration Hub (DIH), plus it can do even more. It provides the architecture as well as orchestration capabilities across all systems—not just backend.

- Digital Bank Operating System (DBOS) connects and at the same time decouples customers’ applications with banks’ internal systems, ensuring seamless interoperability.

- Digital Bank Operating System (DBOS) enables decoupling of digital services from legacy systems.

- Digital Bank Operating System (DBOS) simplifies orchestration across the whole system, not just fragmented backends.

- Digital Bank Operating System (DBOS) accelerates delivery of fast, always-on, cross-channel, cross-segment customer-facing applications.

- Digital Bank Operating System (DBOS) reduces operational risk by centralizing data access and ensuring real-time availability.

The Business Impact: Modernization Without the Pain

Applying the Digital Integration Hub (DIH) approach through the Digital Bank Operating System (DBOS) gives banks a decisive competitive edge: the ability to innovate quickly without disrupting core operations. By decoupling modern digital services from legacy complexity, banks unlock a future-ready architecture while preserving the reliability of their systems of record.

Key business benefits include:

- Faster time-to-market for digital products and features

- Reduced operational risk through centralized, real-time data access

- Improved compliance and audit readiness out of the box

- Enhanced customer experiences across channels and segments

- Future-proofing for AI, personalization, and real-time decisioning

The Digital Bank Operating System (DBOS) turns the Digital Integration Hub (DIH) pattern into a tangible, scalable solution, one that empowers financial institutions to modernize confidently, act with agility, and deliver consistent value to customers.

Closing Thoughts

In a landscape where speed, scale, and experience define winners and losers, clinging to rigid, legacy-bound architectures is no longer viable. With the combined power of the Digital Integration Hub (DIH) and the Digital Bank Operating System (DBOS), banks can chart a smarter course, one that protects what works today while unlocking what’s next.